A good strategy doesn’t not exist in the vacuum imagined by top management, it considers the needs of diverse stakeholders.

In this article, we’ll discuss:

- Part 1. Evolution from the shareholder to stakeholder theory

- Part 2. Stakeholders’ analysis and management in the field of strategic planning

- Part 3. Stakeholders management with BSC Designer software

Part 1. Evolution from the Shareholder to Stakeholder Theory

Do companies exist to generate profits and satisfy the needs of shareholders only?

Should they satisfy the needs of other interested groups?

Let’s track the evolution of business thought in this context.

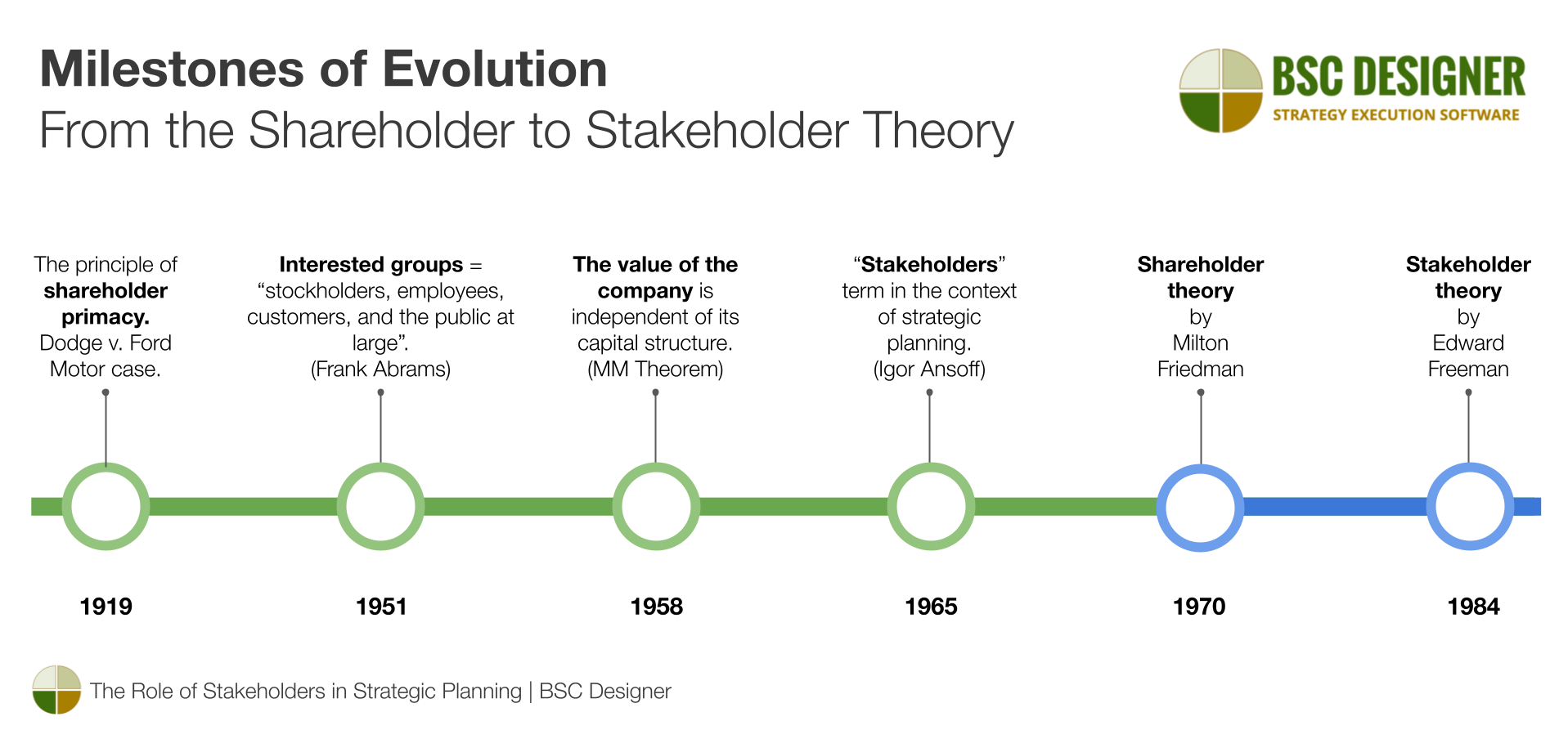

- 1919: Dodge v. Ford Motor case. The principle of shareholder primacy. According to the court decision, Henry Ford had to operate the company for the interests of shareholders, not for the benefit of employees or customers.

- 1951: Frank Abrams, the CEO of Standard Oil of New Jersey, in his article1 used the term “interested groups” to define “stockholders, employees, customers, and the public at large”.

- 1957: Carl Kaysen from Harvard University added2 to the Abrams’s interested groups the firm’s responsibility to itself – organization’s management should “see itself as responsible to stockholders, employees, customers, the general public, and, perhaps most important, the firm itself as an institution”.

- 1958: Modigliani and Miller (MM theorem) stated that the value of the company is independent of its capital structure.

- 1965: Igor Ansoff referred to Abram’s article and introduced the term “stakeholders”3 in the context of strategic planning (according to Wikipedia, the term was used in 1964 in an internal memorandum at the Stanford Research Institute).

- 1970: Milton Friedman introduced4 his shareholder theory or Friedman doctrine.

- 1984: Edward Freeman described the stakeholder theory5.

Shareholder Theory vs. Stakeholder Theory

The discussions about the value of the company expanded far beyond the shareholder or stakeholder theories. In some extreme cases, the argument is that businesses’ main focus should be on solving social challenges… It looks like the critics of the shareholder theory limited their analysis to high-level statements without the intention to reflect on its application under the conditions of current realities.

The author of the stakeholder theory, Edward Freeman, underlines this idea in his interviews. For example, in this short video6, Freeman says that:

- “If Milton Friedman were alive today, he’d be a stakeholder theorist…”

- “What Friedman was against was an idea that social responsibility has anything to do with business – I’m against that too.”

What Theory Does Win in the VUCA World?

We are living in the VUCA world, where the fusion of shareholder/stakeholder theory is the operating system for the current challenges.

While shareholders remain one of the major stakeholders:

- The number and type of other stakeholders are growing to include a more diverse set of interests.

- Organizations are looking to better understand the stakeholders’ landscape of the business environment where they are operating.

For example, watch the latest annual Tesla shareholder meeting. It is a shareholders meeting, but let’s look at the questions in the Q&A part:

- There are many end user’s suggestions about the functionality of the company’s product.

- Attendees discuss ideas about better sustainability of materials and optimizing the supply chain.

- There are questions on the company’s impact on the local community and educating young specialists.

Quantifying Value Value (Gym Case)

With intellectual capital dominating the market, it’s hard to manage the company from the prism of shareholders’ interests only.

Let’s use the idea of a free gym on the company’s site as an example. It sounds like a great idea:

- As confirmed by World Health Organization, physical activity is a leading factor for the employees’ health and emotional state.

- Healthier employees are more productive.

- Informal conversations in gym are expected to generate new connections and ideas.

- The CO2 footprint will be reduced as employees won’t need to drive to a gym.

- With logistics optimized, employees will save their personal time and money.

Let’s try to quantify the value created by the gym using both shareholders and stakeholder theory.

Following shareholder theory, we cannot really quantify the value created for the shareholders. Calculating ROI in this case is a challenge:

- How can we find the dollar value of informal meetings and healthier employees?

- We can track the dynamic of sick days, but this metric is easy to game.

- Some assumptions based on statistical data won’t look good as an argument for the financial reports.

Following the stakeholder theory, we can argue that one of the key stakeholders (employees) will save their personal time, and the gym will help to socialize, and socializing will eventually generate some new ideas for the company.

- We can use “average monthly time saved by an employee” as a value metric.

Hopefully, even in a shareholder-oriented organization, this will be a strong argument to support the gym initiative!

Interesting question is about the viewpoint of the regulator on cases like this… For example, here in Spain, entrepreneurs:

- Can deduce from taxes reactive healthcare measures (private medical insurance), but

- Cannot deduce the proactive healthcare measures (like the costs of the gym’s subscription).

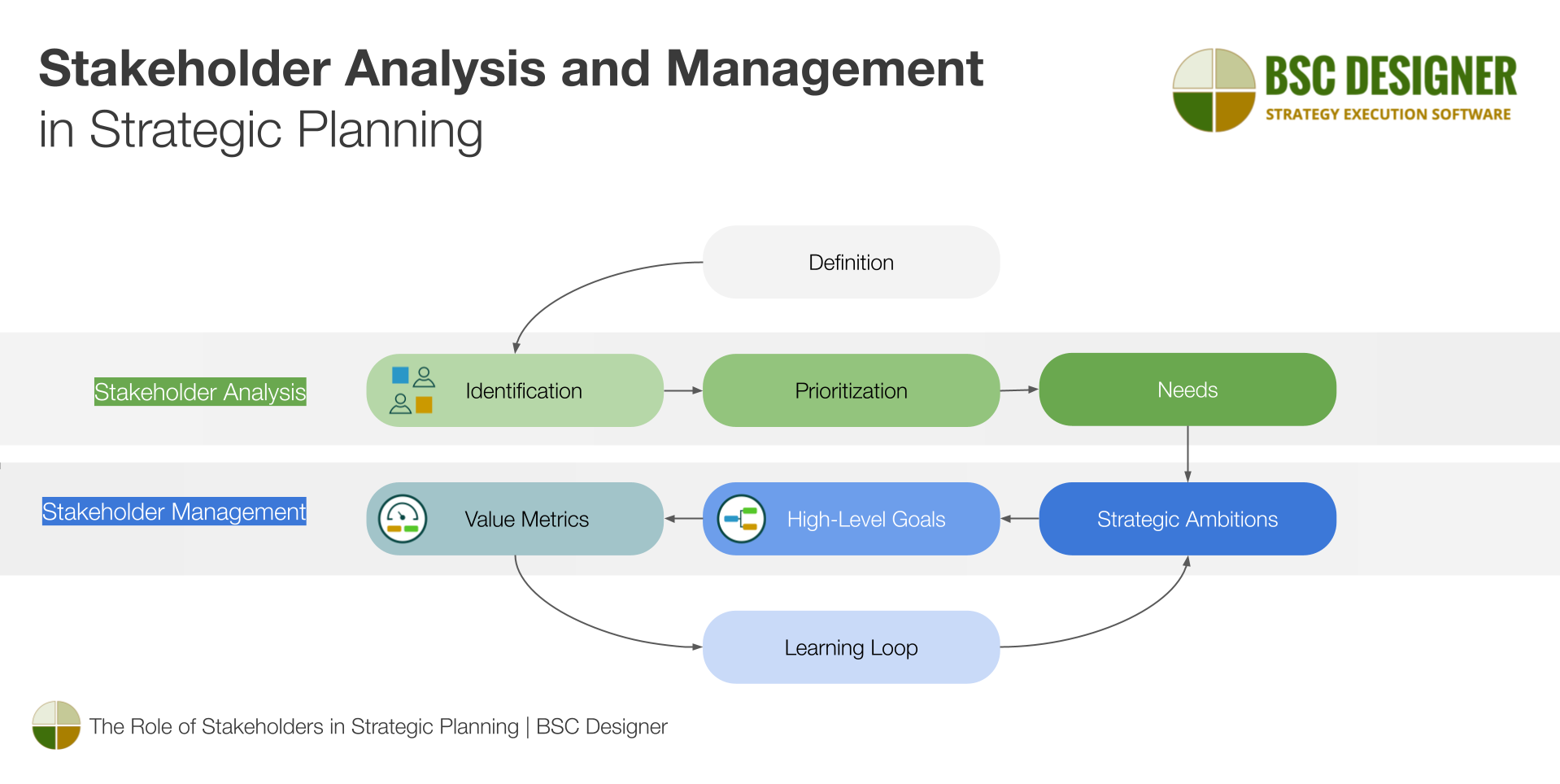

Part 2. Stakeholder Analysis and Management in Strategic Planning

The goal of stakeholder analysis is to:

- Identify the stakeholders

- Explore their needs, and

- Prioritize.

The stakeholder management in strategic planning7 refers to:

- Formulating strategic assumptions according to the needs of stakeholders.

- Splitting up high-level goals into subgoals.

- Quantifying subgoals by the value for stakeholders.

- Validating achievements with stakeholders.

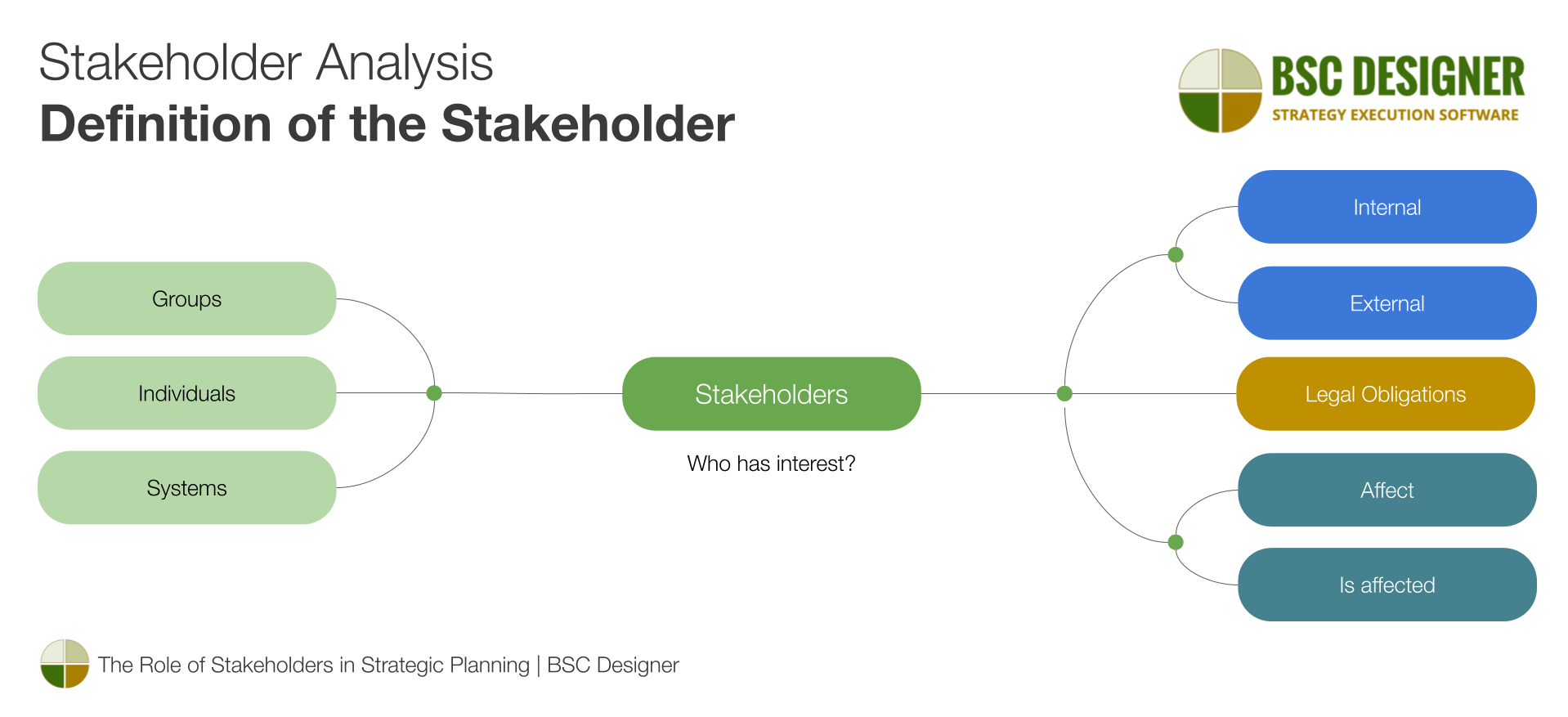

Stakeholder Analysis: Definition of the Stakeholder

Here are some definitions of the stakeholder term:

- Edward Freeman, 19838: “Groups without whose support the organization would cease to exist.”

- ISO 26000: “Individual or group that has an interest in any decision or activity of an organization.”

- Tom Gilb, 2019: “Stakeholders are any person, group or system, that have or we want to have an interest in our project.”

- European Sustainability Reporting Standard, 2023: “Individuals or groups whose interests are affected or could be affected – positively or negatively – by the undertaking’s activities and its direct and indirect business relationships across its value chain.”

Stakeholder Analysis: Identification of the Stakeholders

Start with stakeholders defined by Business Roundtable:

- Customers

- Employees

- Suppliers

- Communities, and

- Investors

Check if there are any legal obligations about the stakeholders. For example, European Sustainability Reporting Directive introduced two additional groups of stakeholders in the context of sustainability reporting:

- “Affected Stakeholders” and

- “Users of Sustainability Statements”

To add more stakeholders to the list, look at the definition of the stakeholders and ask corresponding questions:

- Who has interest in our organization?

- Who is affected or might be by our organization?

- Who affects or might affect our organization?

Here are some examples from different business domains:

- Stakeholders of procurement department

- Stakeholders in corporate governance

- Stakeholders of university strategy

When answering these questions:

- Look at the groups, individuals, systems…

- Consider internal and external stakeholders.

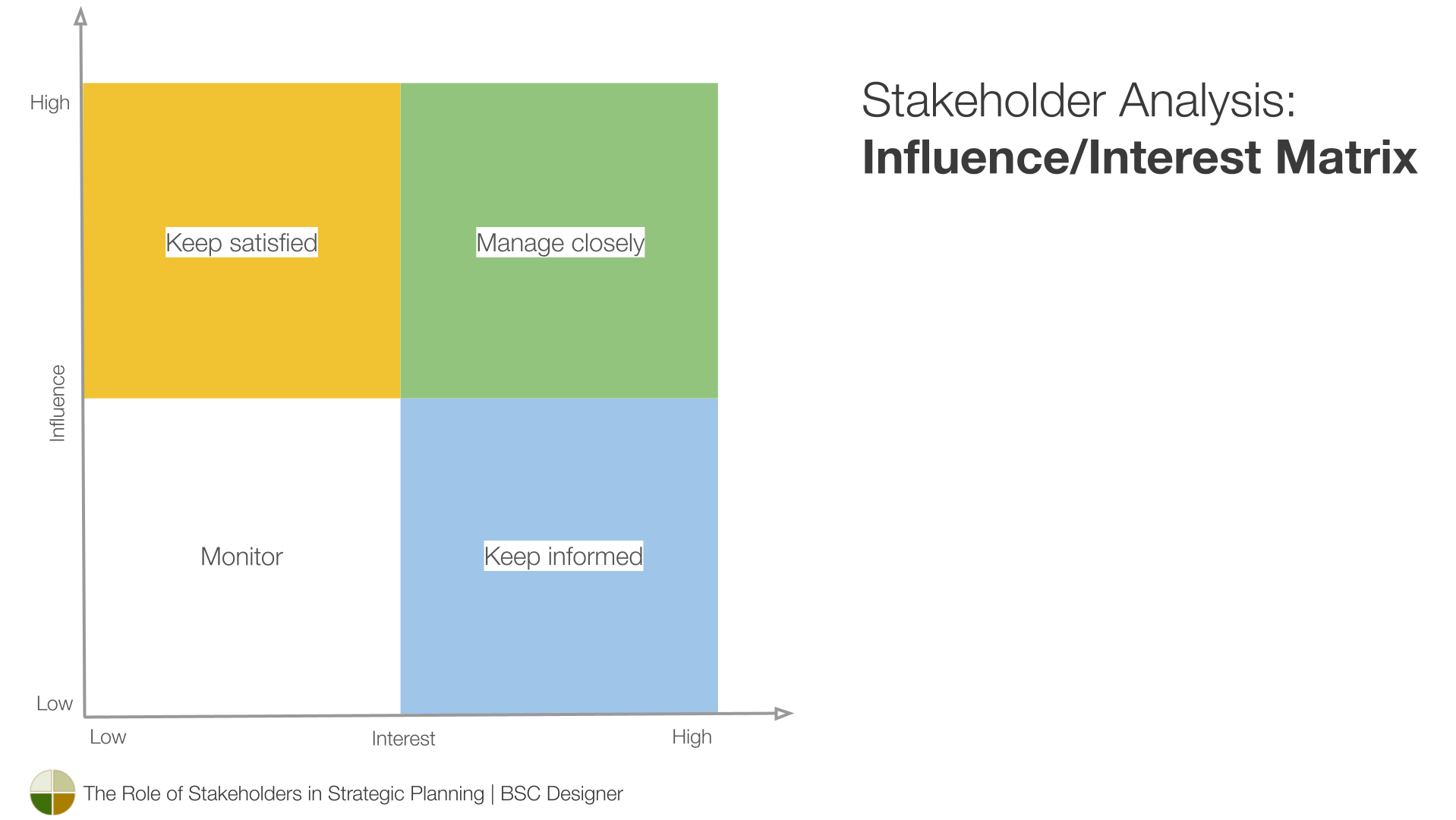

Stakeholder Analysis: Influence/Interest Matrix

With limited resources of organization, we need to prioritize attention to the stakeholders and their needs. A classical tool for this purpose is the 2×2 influence/interest (or power/interest) matrix.

Depending on the sector of the diagram where the stakeholder belongs to, the organization decides a response strategy:

- Manage closely the stakeholders from the high influence/high interest quadrant.

- Keep satisfied the stakeholders from the high influence/low interest.

- Keep informed the stakeholders from the low influence/high interest quadrants.

- Monitor the stakeholders from the low influence/low interest quadrant.

The limitations of the matrix approach are:

- The subjectiveness of the classification

- The vague ideas of “manage” and “keep satisfied”

We partially mitigate these limitations by quantifying the value for the stakeholders and following a disciplined strategic planning approach.

Stakeholder Analysis: Assumption About the Needs of the Stakeholders

Once the list of stakeholders is defined, we need to understand their:

- Needs/interests

And any relevant properties like:

- Resources

- Priorities

- Constraints

Even if we do face-to-face interviews and ask specific questions, the stakeholders’ answers will be subjective and contradictory.

The results of stakeholder analysis will always be an overlap of what stakeholders shared and the experience of your team.

Stakeholder Management: Using Results of Analysis in Strategic Planning

Stakeholders’ definition and analysis is an input for strategic planning and related disciplines:

- We use stakeholders’ definition in value base strategy decomposition.

- We use their strategic ambitions to formulate and execute with complex strategies.

- We define stakeholders to quantify the quality (even the qualities of AI), focus the digital transformation efforts.

- We do stakeholders analysis to comply with regulatory reporting.

Considering the needs of stakeholders and their position in the influence/interest matrix, we need to decide whether the strategic ambitions of the stakeholders resonate with existing strategy.

We’ll use the interests of shortlisted stakeholders to:

- Formulate stakeholder’s strategic ambition

- Resolve conflicting ambitions

- Formulate high-level goals

- Split up high-level goals into subgoals

- Quantify the subgoals by the value for the stakeholders

The strategic ambition of the stakeholder is not absolute truth – similar to any other hypothesis we need to validate it in execution.

We do it by establishing learning loop:

- Tracking value indicators and

- Getting early feedback from the stakeholders.

Find more details in our guide on implementing strategy in a complex environment.

Stakeholder Analysis and Management: Example

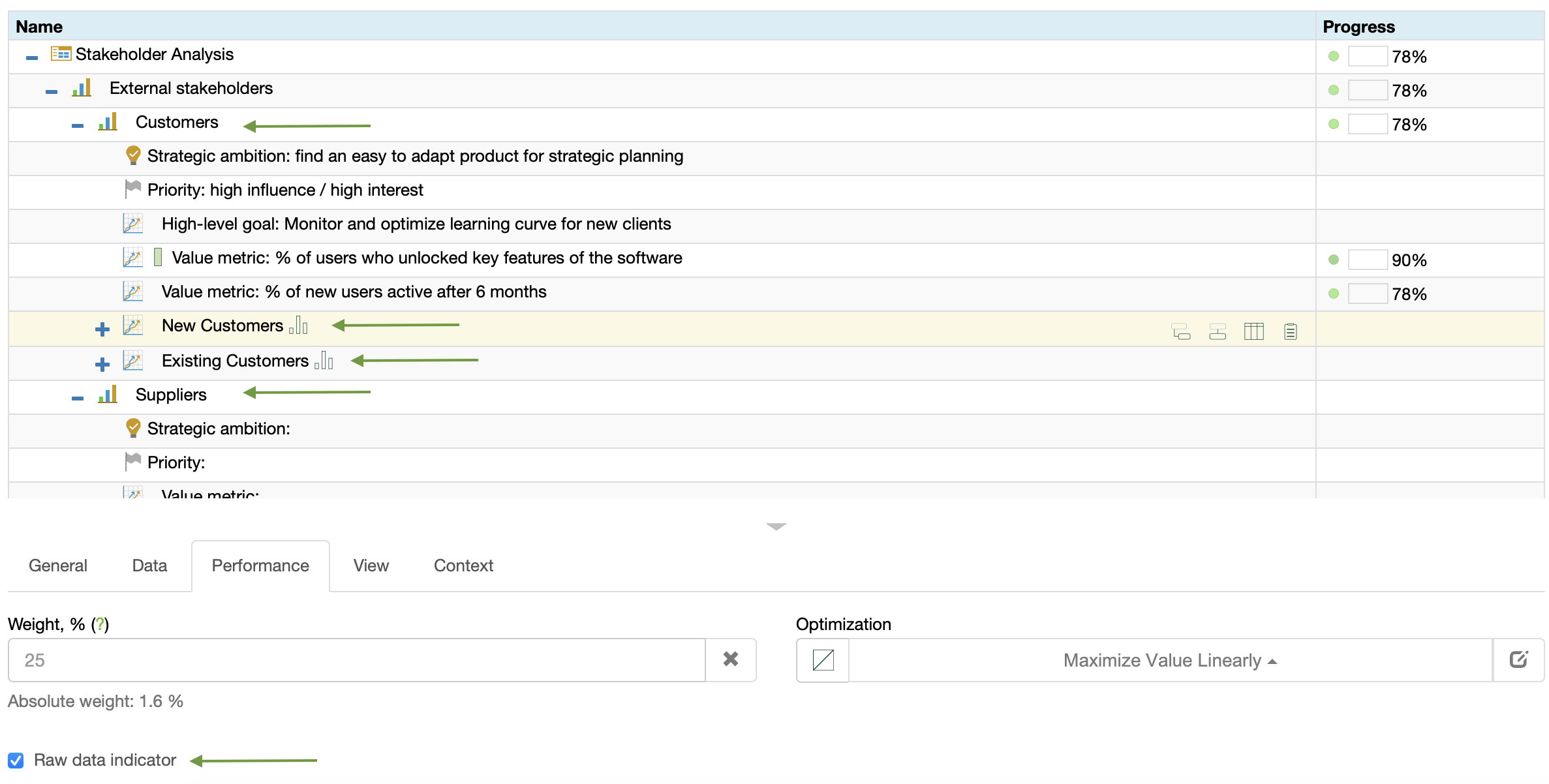

To illustrate the stakeholder analysis and management, let’s use the example of the BSC Designer’ s stakeholder group defined as “new customers”.

Stakeholder Analysis:

- Stakeholder: new customers

- Definition: customers who have signed-up with the free plan within the last 2 weeks.

- Stakeholder needs: understand if/how the tool solves their challenges of strategic planning (see the Stage 1 – Testing waters).

- Stakeholder resources/constraints: time constraint to shortlist the strategic planning tools; budget to buy a subscription.

- Stakeholder priorities: find the tool that is viable to automate the strategic planning methodology implemented in their organization that requires minimal adoption time.

- Prioritization: high influence / high interest.

Stakeholder Management:

- Strategic ambition of stakeholders: “Find an easy to try and adapt product for strategic planning.”

- High-level goal of BSC Designer: “Monitor and optimize learning curve for new clients.”

- Value (leading) metric: % of new users who unlocked key features of the software.

- Value (lagging) metric: % of new users active after 6 months.

- Value (lagging) metric: % of new users converted to a business plan.

- Learning loop: analysis of the challenging functions for the beginner; validating improvement ideas with new customers.

Practical notes:

- The stakeholders analysis is compatible with other strategic planning tools, like, for example, the competitive analysis framework Five Forces.

Part 3. Stakeholders management with BSC Designer Software

This chapter will be useful for those who use BSC Designer to automate their strategic planning. If you are not a user of BSC Designer yet, sign-up with a free plan to start building prototypes of your strategy scorecards.

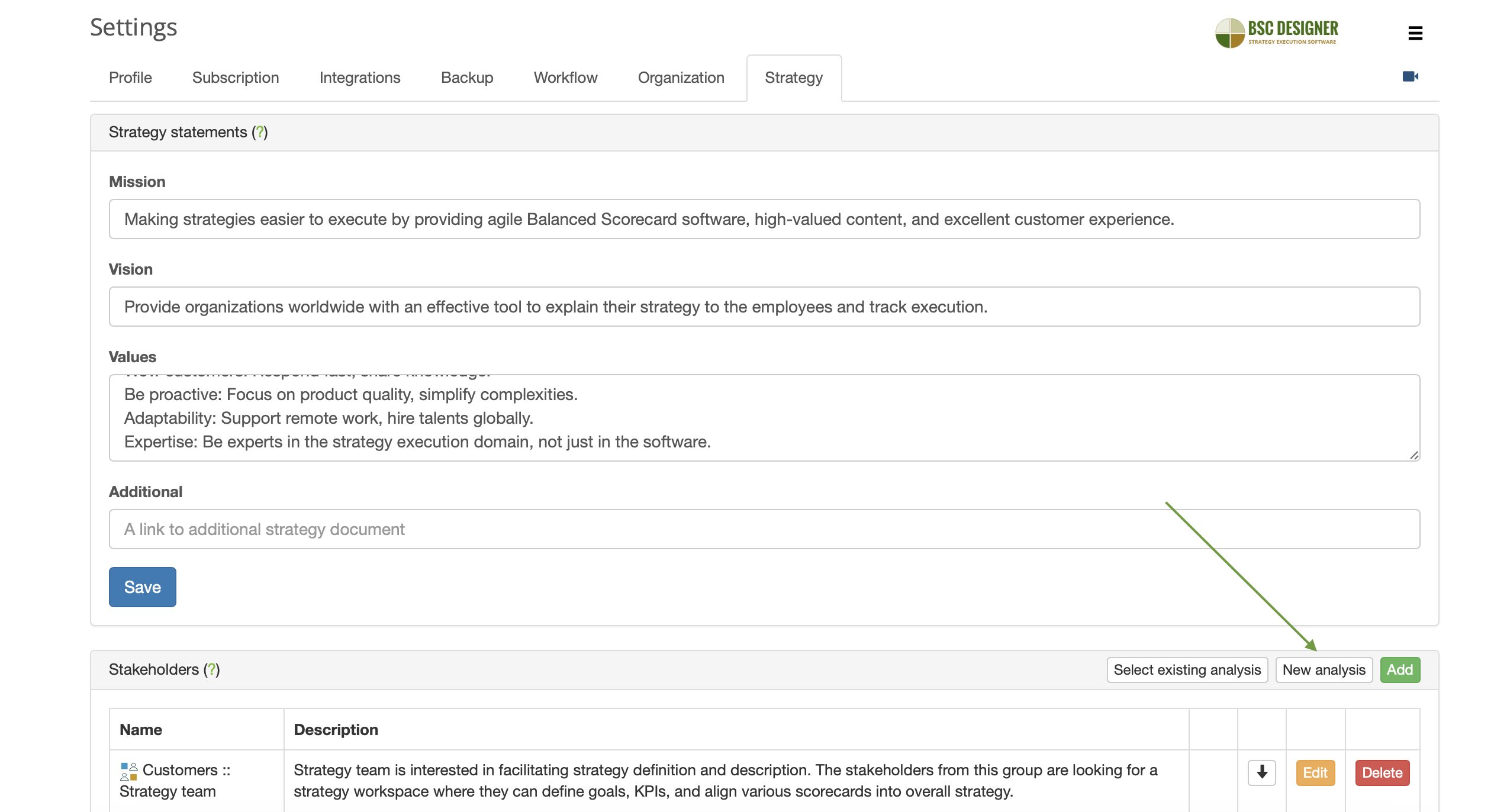

Stakeholders Analysis

Use the Stakeholder Analysis template available in BSC Designer to identify stakeholders, their strategic ambitions, priorities, and metrics for quantifying value.

To use the template:

- Navigate to Menu > Settings > Strategy tab.

- Click on the New analysis

- Access the created stakeholder analysis template by clicking on its name:

- Add stakeholders to the template or make modifications to existing ones:

The software will recognize all items on the third level as stakeholders. If you need to add sub-groups for stakeholders, use the ‘raw data’ checkbox on the Performance tab:

- Once finished, go back to Settings > Strategy and click the Sync button to load the outcomes of the analysis into the list of stakeholders.

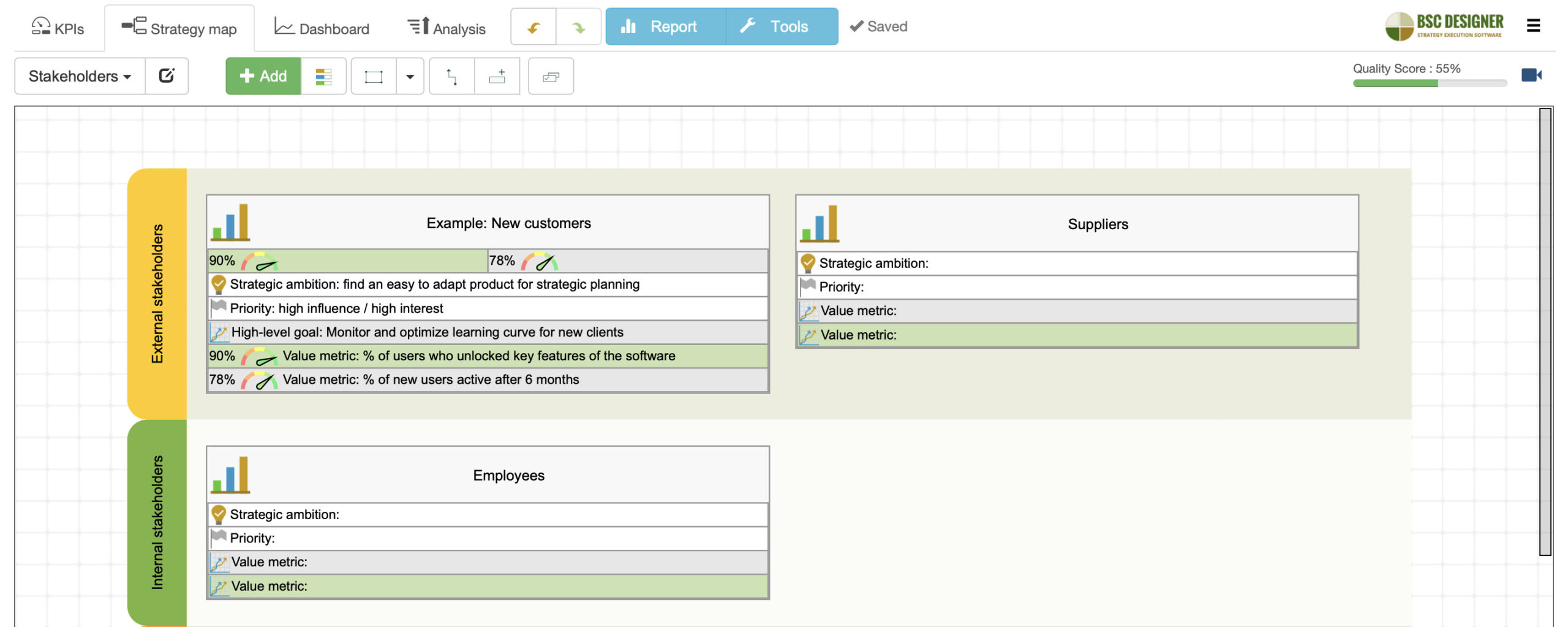

Align Stakeholders with the Goals

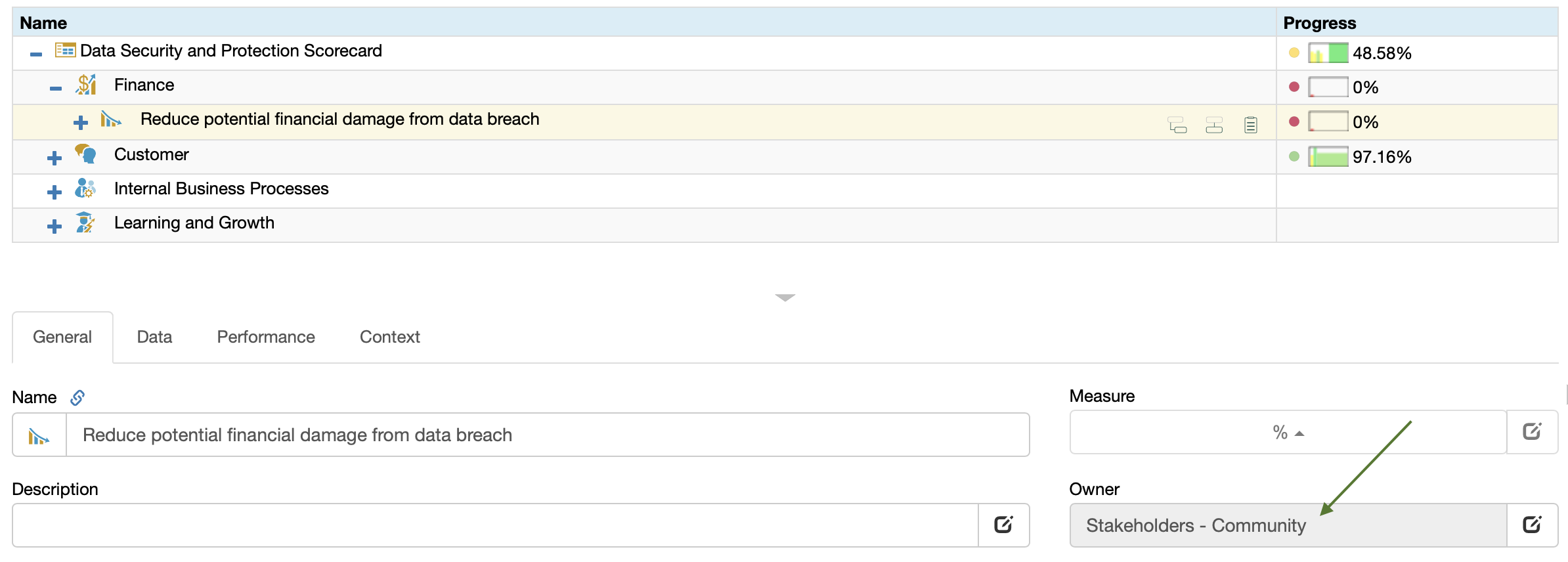

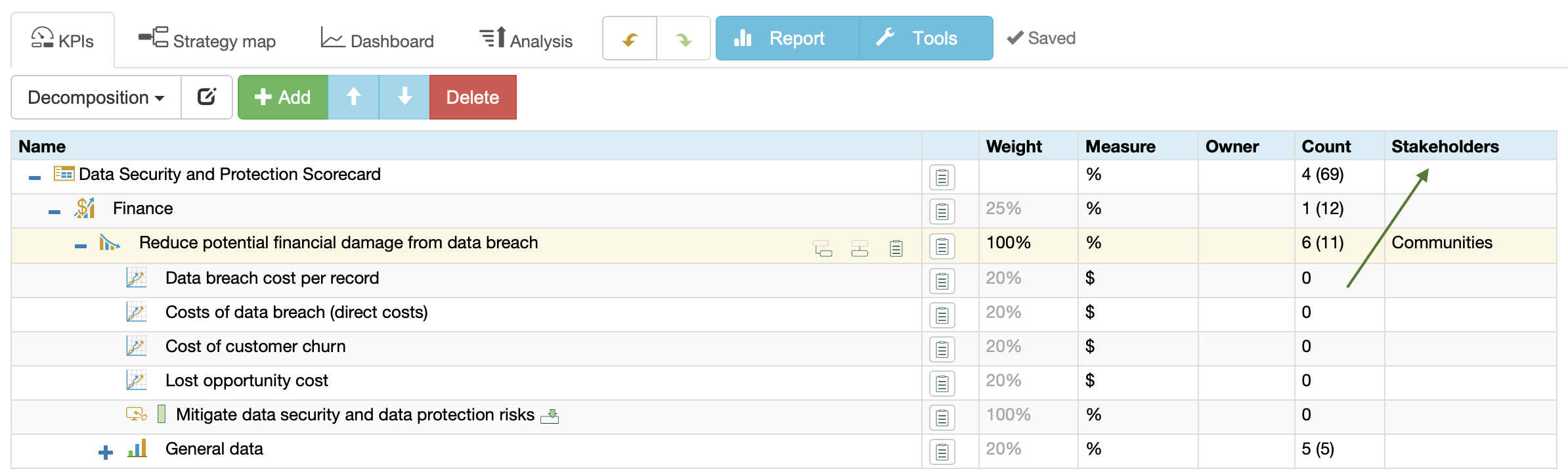

The practical benefit of having the list of the stakeholders in the software is that you can assign the stakeholders to specific goals and KPIs using the Owner field.

The software will visualize stakeholders relevant for the goals/KPIs:

- On the KPIs tab (depending on the chosen view)

- In the reports

- On the dashboard

For internal stakeholders, for example, your strategy team, use the Menu > Users section.

- The stakeholders in the software are for contextual purposes only (displayed in the interface and in the reports),

- The users, in contrast, can be actively engaged in strategic planning – have access to the scorecards, enter new goals, new data, and receive notifications.

Quantify the Value Created for the Stakeholders

Quantify the goals with the value for stakeholders.

- Align leading and lagging indicators with the goal (change the indicator’s type on the Context tab)

- The stakeholders aligned with the goal can be displayed in the Stakeholders column or Owner field

Cost Reduction Strategy and AI

Consider using generative AI for Cost Reduction Strategy. In this article, we discuss the steps to use the output of AI in strategic planning automated with BSC Designer. We also share some thoughts about the security and privacy concerns.Takeaways

Stakeholders are groups or individuals who have interest or are affected by the organization.

While shareholders are the main group of stakeholders, for effective strategy definition and execution, strategists need to:

- Analyze stakeholders and their needs,

- Prioritize their influence/interests,

- Convert strategic ambitions of the stakeholders into high-level strategic goals.

On the practical level:

- The connection between the needs of the stakeholders and strategy is established via the leading and lagging indicators that quantify the value for the stakeholders.

- Getting early feedback from the stakeholders and adjusting strategy accordingly is critical for successful strategy execution.

- Management’s Responsibilities in a Complex World, Abraham, F. W., 1951, HBR ↩

- The Social Significance of the Modern Corporation, Carl Kaysen, American Economic Review 47, 1957 ↩

- Corporate Strategy: An Analytic Approach to Business Policy for Growth and Expansion, H. Igor Ansoff, McGraw-Hill, 1965 ↩

- A Friedman doctrine – The Social Responsibility Of Business is to Increase its Profits, Milton Friedman, The New York Times, 1970 ↩

- Strategic management: a stakeholder approach, R. Edward Freeman, Pitman, Boston, 1984 ↩

- Shareholders vs. Stakeholders — Friedman vs. Freeman Debate – R. Edward Freeman, https://www.youtube.com/watch?v=_sNKIEzYM7M ↩

- “Strategic Planning Process: Mission, Priorities, Goals, KPIs, Initiatives,” BSC Designer, June 18, 2019, Aleksey Savkin, https://bscdesigner.com/strategic-planning-process.htm. ↩

- Stockholders and Stakeholders: A new perspective on Corporate Governance, California Management Review, 1983 ↩

![]() CEO | Author | Speaker

CEO | Author | Speaker

BSC Designer is strategy execution software that enhances strategy formulation and execution through tangible KPIs. Our proprietary strategy implementation system reflects our practical experience in the strategy domain.