As a part of the EU Green Deal, new reporting standards and directives have been introduced. While the adoption is challenging due to the complexity of the new standards, in their core, new requirements focus on the best practices of strategic planning and reporting, such as mapping stakeholders, objectives, key activities, risks, tracking leading and lagging performance indicators.

We’ll discuss how to prepare strategy scorecards for sustainability reporting and align them according to the ESRS 1, ESRS 2 and Topical Standards.

This article will be useful for:

- Users of BSC Designer who already track their sustainability strategies / KPIs with the software and want to prepare for the reporting according to the new sustainability standards.

- Sustainability consultancies interested in automating reporting for their clients.

High-Level Requirements of the CSRD

9 June 2023, the European Commission published the first drafts of sustainability reporting standards (ESRS) that will eventually form part of the Corporate Sustainability Reporting Directive (CSRD).

Summarizing the requirements of the standards, we can formulate the following high-level disclose requirements:

- Stakeholders. Have a list of stakeholders that must include two groups – affected stakeholders and the users of sustainability statements (investors, partners, governments).

- Strategy mapping. Have necessary contextual information for the strategies, key activities, risks, performance indicators (basically, describing the properties of a classical strategy map).

- Performance measurement. Track the degree to which the policies were implemented (leading indicators), track results in the context of the affected environment (lagging indicators).

- Double materiality. Track the impact of sustainability matters on the organization and the impact of the organization on the environment.

- Alignment between strategy and functional scorecards. According to the ESRS 1 and ESRS 2, the scope of the reporting includes governance, high-level strategy, and reporting according to the topical standards.

Below, we discuss how to implement the mentioned disclosure requirements in practice and how their terminology match strategic planning.

Affected Stakeholders and Users of Sustainability Statements

The standard suggested a broad definition for the stakeholders, dividing them into two groups:

- Affected stakeholders (stakeholders affected positively or negatively, across all value chain)

- Users of sustainability statements (investors, partners, governments, etc.)

The standard recognizes that some stakeholders might belong to both groups at the same time.

In strategic planning, we start with the definition of stakeholders and their needs. The practical recommendation is to:

- Revise the list of existing stakeholders, adding the types of stakeholders according to the requirements of the standard.

- In the description for the stakeholder group, make a note about their belonging to one of the groups or both.

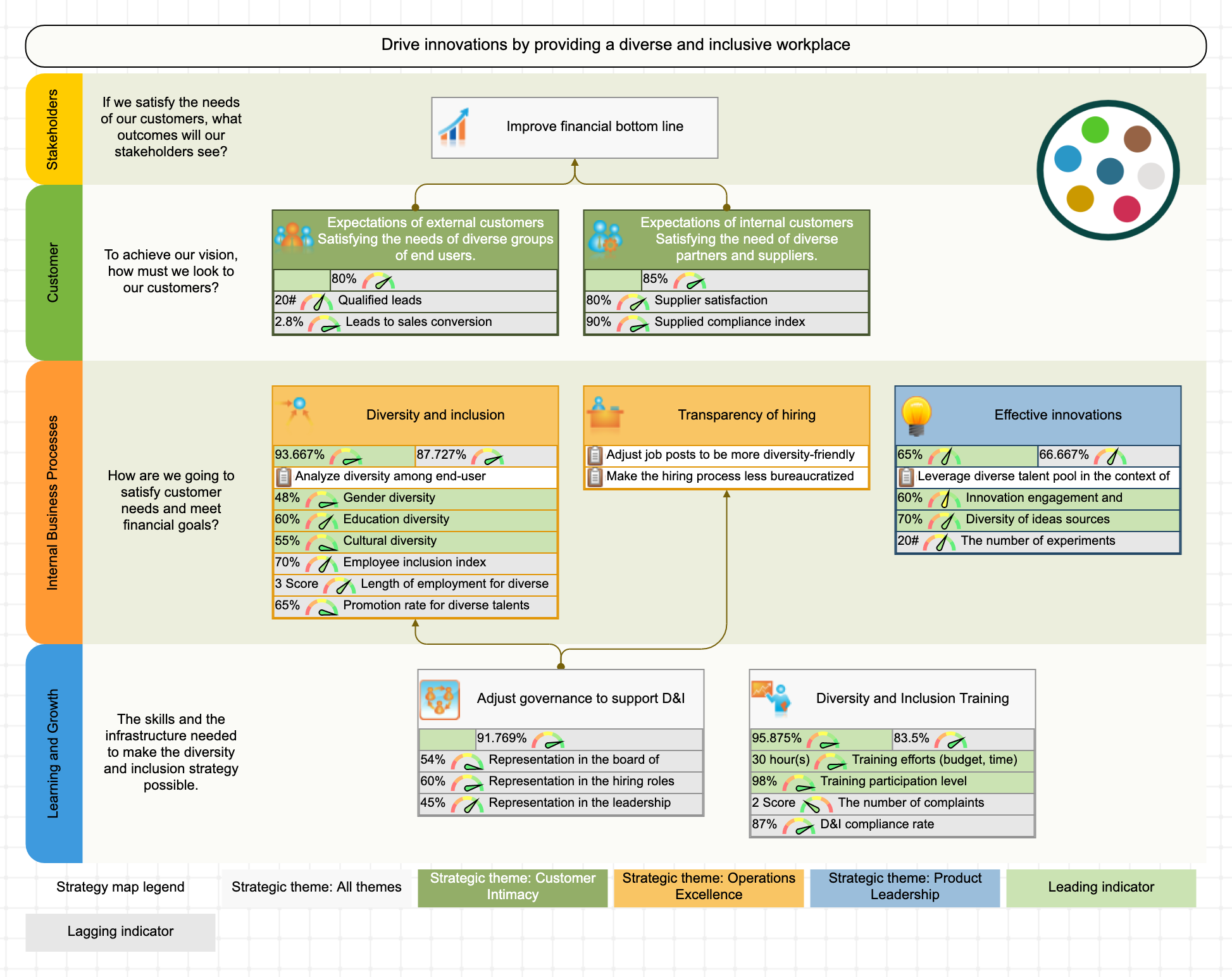

Reporting Areas – Best Practices of Strategy Map

The term “strategy map” is not used in the standard, but looking at the “1.2 Reporting areas and minimum content disclosure requirements on policies, actions, targets and metrics,” we will see typical properties of the strategy map:

- Mapping strategy/goals

- Risks

- Contextual information

- Metrics with targets

- Policies and actions (initiatives)

With properly designed strategy scorecards and their respective strategy maps, an organization has the necessary tools to present and report strategy as required by the standard.

Nevertheless, those strategy maps will fulfill their main function: support informed discussions around the strategy, help with strategy execution, facilitate discussion with stakeholders.

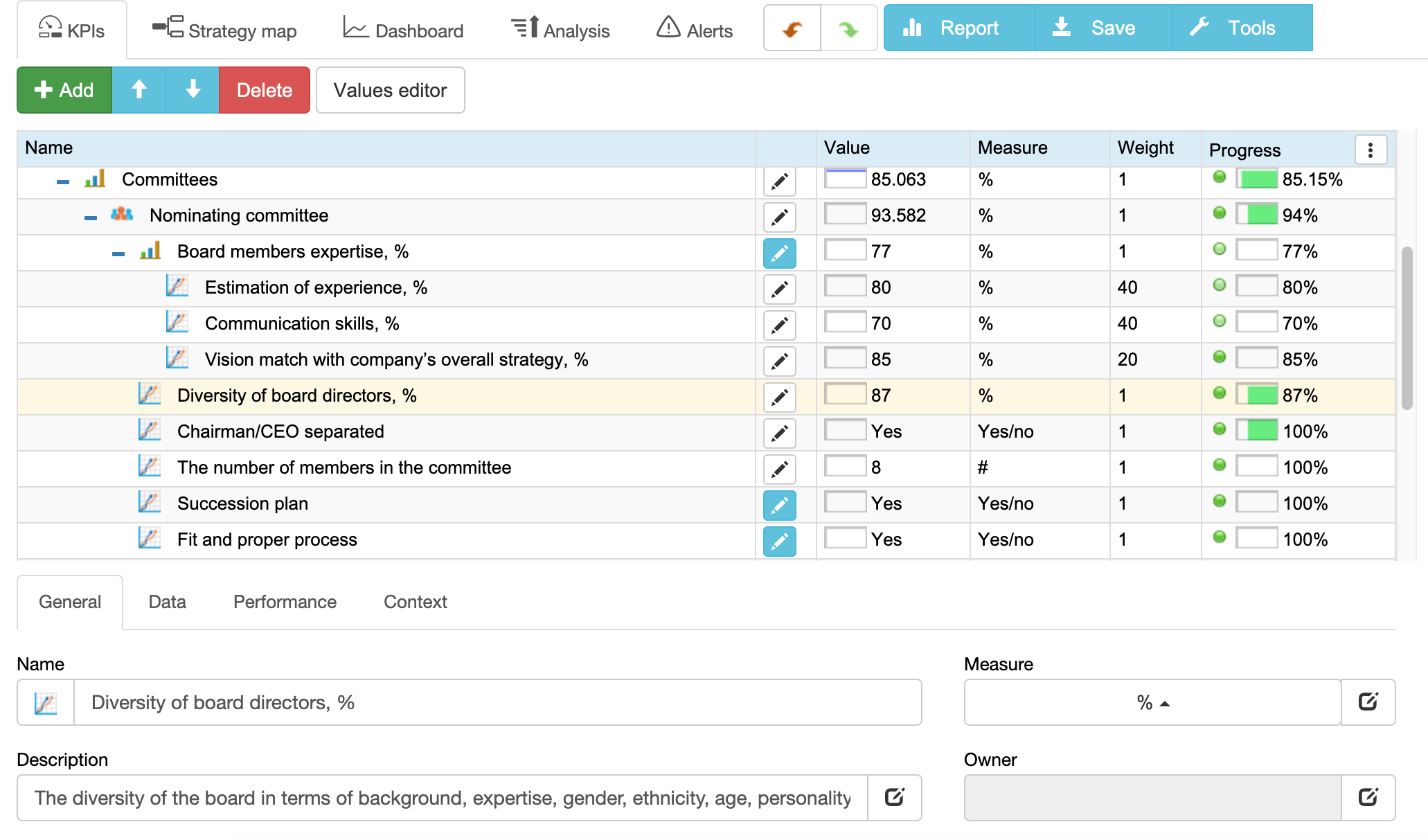

Metrics and Targets – Performance Reporting

As we can conclude from the definition given for the “metric” (see ANNEX II Acronyms And Glossary of Terms), from the viewpoint of the standard metrics:

- Can be quantitative and qualitative.

- Should measure the effectiveness of sustainability-related policies (leading metrics).

- Should measure results in the context of affected environment (lagging metrics).

- Should be tracked over time.

With a strategy scorecard automated by BSC Designer, the mentioned requirements are delivered out-of-the-box. Users of BSC Designer:

- Can define quantitative and qualitative measurements units.

- Have native support for leading and lagging indicators (see the “Type” property on the “Context” tab).

- Track the data for the indicators over specified reporting periods (monthly, quarterly, annually, etc.).

- Have additional automation functions, including notifications, reporting, import/export, visualization on dashboards.

Double Materiality – Measuring Impact on Organization and Impact of the Organization

The standard established the principle of double materiality (see ANNEX II Acronyms And Glossary of Terms), dividing it into:

- Financial materiality – the impact of sustainability matter on the organization

- Impact materiality – the impact of organization on the environment

Under the umbrella of Financial Materiality, organizations should consider:

- Risk and opportunities that affect or could reasonably affect the financial perspective over the short, medium or long term.

The Impact Materiality covers impact on environment that is:

- Actual or potential

- Positive or negative

- Short, medium or long term

- Related to own operations and value chain

From a practical perspective, the requirements of the standard extend the scope of measurement. The double materiality idea can be automated as two separate scorecards, one dedicated to the financial materiality and another to the impact materiality.

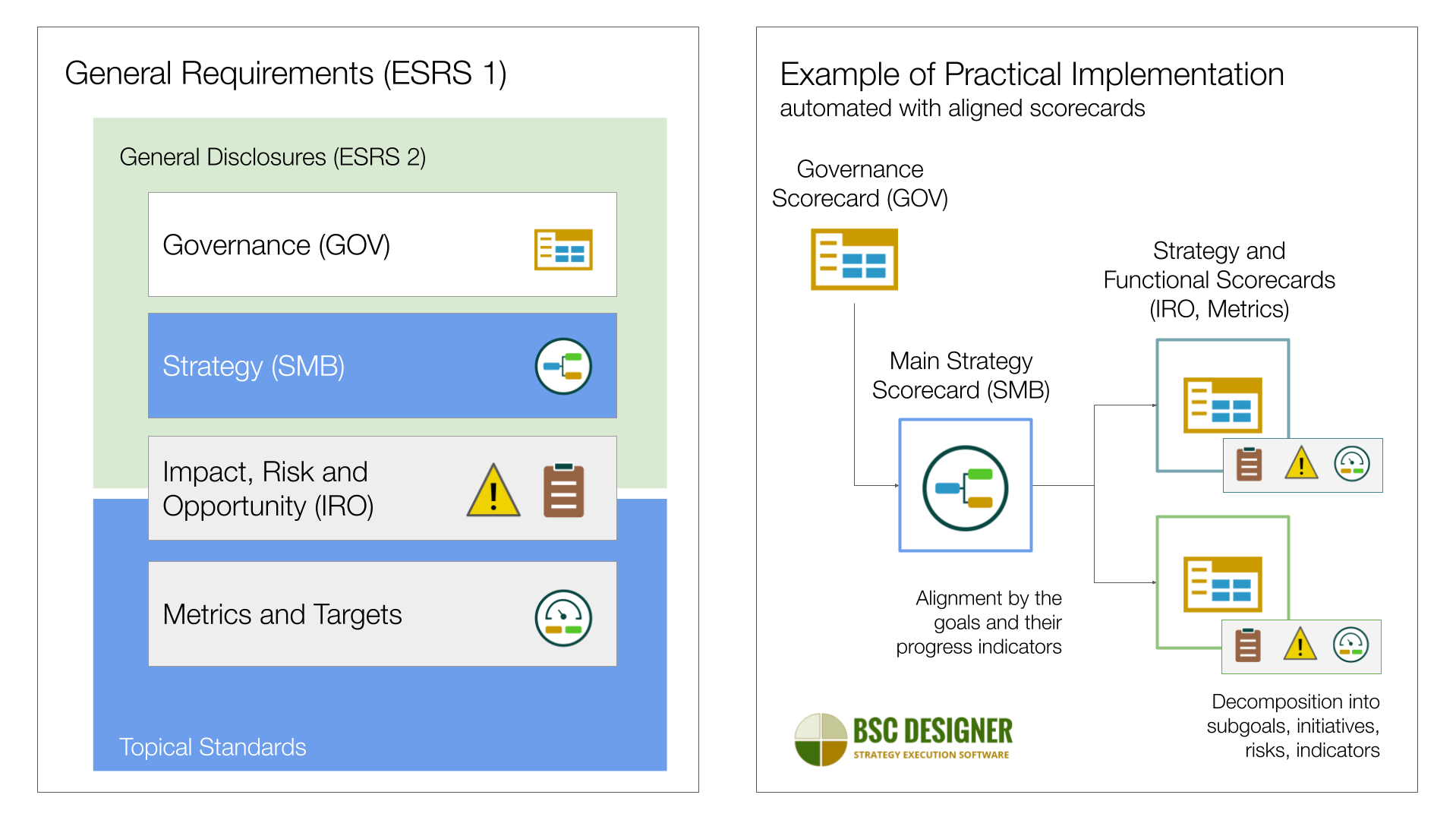

Aligning Strategy Scorecards – Interaction of ESRS 1 and ESRS 2

As articulated in the ESRS 1 and ESRS 2, reporting is required on the levels of:

- Governance (GOV – ESRS 2 – General Disclosures)

- Strategy (SBM – ESRS 2 – General Disclosures)

- Impact, Risk, Opportunity (IRO – ESRS 2 – General Disclosures and Topical Standards) with reporting on policies and action plans

- Metrics and Targets (Topical standards) with reporting on progress and effectiveness

Users of BSC Designer can organize respective reporting scorecards via a number of aligned scorecards:

- Governance scorecard as a key strategy scorecard (see the template of governance scorecard).

- Strategy scorecards to describe the overall strategy, as well as specific sub-strategies with their respective goals, risks, and opportunities (see the guide for implementing strategy in complex environment).

- Functional scorecards will correspond to the disclosures according to the topical standards.

- The progress outcomes of the functional scorecards can be used as inputs for the strategy scorecards.

Conclusions

Properly organized strategy and functional scorecards facilitate the reporting of the organization according to the new reporting standards and disclose requirements.

The adoption roadmap should include:

- Revision of the list of stakeholders to add affected parties and users of sustainability statements.

- By following the best practices of strategy mapping, organizations prepare necessary contextual, risk, and performance information for the reporting according to the new standards.

- The requirement to have leading and lagging indicators in the scorecards can no longer be ignored. In addition to other measurement requirements, the new standard is clear about measuring the effectiveness of policies (quantified by leading indicators) and results in the context of affected requirements (lagging indicators).

- The measurement and reporting scope should be extended according to the double materiality, measuring not only the impact of the organization on the environment but impact on the organization as well.

- The directive requires reporting according to the broad range of areas: Governance, Strategy (ESRS2), Risks, Metrics, and Targets (Topical Standards). On a practical level, these reporting areas can be automated via a number of aligned strategy and functional scorecards.

While the new standards are focused on larger organizations, SMBs will benefit from adopting general principles of sustainable reporting (see the alignment with SDGs as an example).

BSC Designer is a strategy execution software that will support users on all stages of strategy definition, description, and execution, including definition of the stakeholders, mapping goals, tracking leading and lagging indicators with their targets, aligning strategy and functional scorecards.

![]() CEO | Author | Speaker

CEO | Author | Speaker

BSC Designer is strategy execution software that enhances strategy formulation and execution through tangible KPIs. Our proprietary strategy implementation system reflects our practical experience in the strategy domain.